The definition of Innovation Accounting Innovation Accounting is “an organized system of principles and indicators designed to gather, classify, analyze and report data about a company’s breakthrough and disruptive innovation efforts – working to complement the existing financial accounting system.” From “Innovation Accounting, a practical guide for measuring your innovation ecosystem’s performance” Why do we […]

Innovation Accounting: how to measure innovation success

Manage the development of new products and business models and align innovation with your business strategy, by applying innovation accounting to your innovation ecosystem.

Table of Contents

Levels of Innovation Accounting

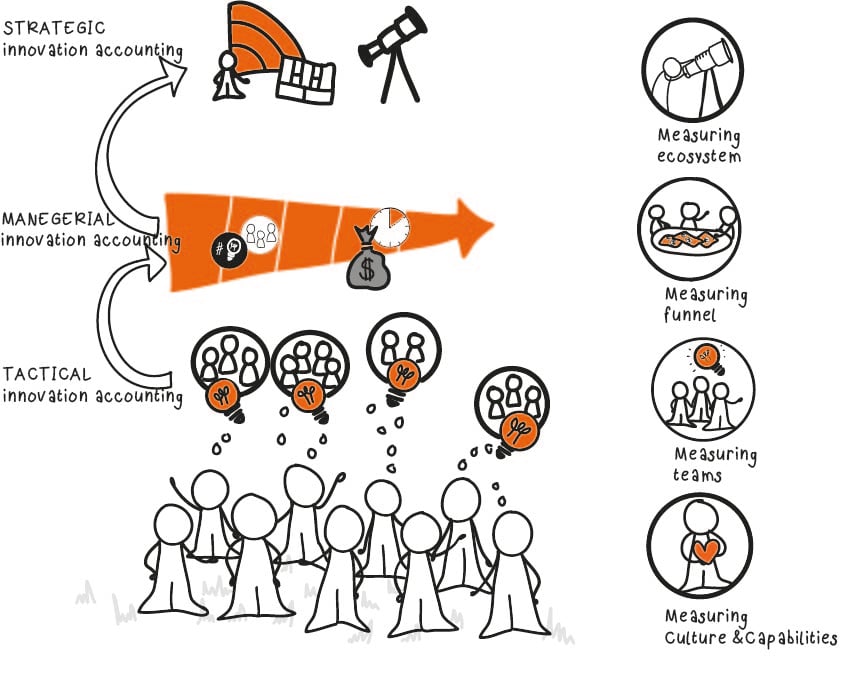

Within the innovation accounting framework, there are three layers of indicators that feed one into the other. It gathers data on an individual venture level to make sure that investment decisions are being made through data rather than gut feeling. That data is aggregated to make sure there is insight in the entire funnel of ventures and abstracted again to translate into strategic indicators relevant for the board and the overall strategy of the company.

- Tactical innovation accounting is connected to Measuring teams. These focus on product teams, the experiments they are running, the learnings they are having, and the progress they are making from ideation to scale.

Read more: 3 Reporting KPIs to get started with innovation accounting - Managerial innovation accounting is connected to Measuring funnel. The focus here is on helping the company make informed investment decisions based on evidence and the current innovation stages teams are in.

- Strategic innovation accounting is connected to Measuring ecosystem. The focus here is on helping a company's board examine the overall performance of their investments in innovation in the context of the larger business, connecting to overall strategy as well as decisions on capability and culture.

In order to measure your whole innovation ecosystem, and get the most accurate, reliant, and timely data, we encourage you to also measure:

- The startup collaborations to better manage your collaboration projects and maximize the value of the partnership between corporations and startups.

- Innovation HR capabilities to make sure you have the right mix of people with the right skillsets.

- Innovation culture to make sure that your organization has a setting in which innovation can drive.

Types of Innovation Accounting Metrics

Besides the different levels of Innovation Accounting, there are also two different types of innovation metrics:

Performance indicators focus on how well the teams are doing in regard to the innovation process.

In contrast, Result indicators measure the tangible results that are emerging from this innovation activity.

Innovation Labs have the tendency to focus on performance metrics rather than result metrics. That is fine to show early signs of success, but in the end, innovation has to have a real impact on the organization. Taking result metrics into account is not benchmarking the results with industry standards, it is looking at what the numbers are telling us, are they indicating a possible sustainable, repeatable, and scalable business model? It is wise to look at both performance and result indicators at every stage of the innovation framework.

Set up your own Innovation Accounting

with GroundControl as your single source of truth

Designed for Innovation Managers and Corporate Ventures

Innovation Managers

- Have real-time insights into the performance of their innovation program with innovation accounting.

- Have a visual overview of the progress of all ventures.

- Can report with confidence to the board with clear and visual data.

Corporate Ventures

- Easily identify their riskiest assumptions, thanks to clear key questions and a smart risk model.

- No more PowerPoint! Generate One-Pagers based on factual data and learnings.

- Use shared learnings from other ventures.

Innovation Accounting Infographic

We created a printable infographic poster of everything there is to know about innovation accounting. You can download and print it for free.

Download Innovation Accounting infographic

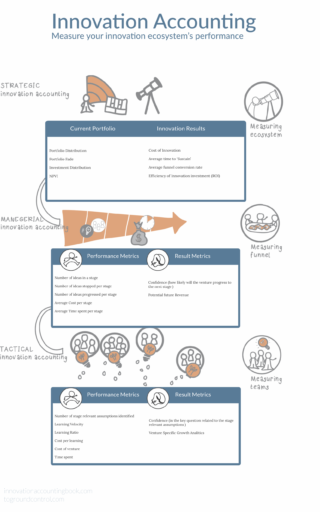

Download Innovation Accounting infographicExample metrics for Tactical innovation accounting

Performance Metrics |

Result Metrics |

|---|---|

|

|

- Number of stage-relevant assumptions identified.

- Learning velocity: during a specific time period, how many learnings in the form of insights did the team acquire that provided valuable information about the problem and the target customer group?

- Learning ratio: The learning ratio provides insight into the speed at which the team is acquiring new knowledge. It is calculated by dividing the number of successful experiments by the total number of experiments conducted.

- Cost per learning: what was the expense incurred by the team for each learning? This cost includes not only the time invested per learning but also other expenses related to activities like traveling expenses, ethnographic work, facilitated workshops, or materials etc.

- Cost of venture:

- Time spent

- Confidence: the level of certainty the team has that the identified problem is worth solving. To gauge this, the team engages in regular, open discussions based on the empathy work conducted in the field. These conversations revolve around assessing the likelihood of the uncovered problem being a genuine issue for the specific target group, rather than just a desirable but non-essential aspect.

- Venture specific growth analysis:

Example metrics for Managerial innovation accounting

Performance Metrics |

Result Metrics |

|---|---|

|

|

- Number of ideas in each stage: this is a straightforward tally of the number of ideas being developed at each stage of the Product Lifecycle.

- Number of ideas stopped per stage: Tracking the number of ideas that have been discontinued and identifying the specific stages at which they stopped provides valuable insights into an organization's innovation maturity.

- Number of ideas progressed per stage: the number of ideas that successfully advance to the next stage, helps organizations gain insights into the health and effectiveness of their innovation pipeline.

- Average cost per stage: illustrates the financial investment made by the company at each stage of the Product Lifecycle.

- Average time spent per stage: this metric provides valuable insights into the speed at which ventures progress from one stage to the next or are discontinued. Organizations can assess the efficiency of their innovation process and identify areas where improvements can be made to expedite or streamline the venture's journey through different stages.

- Confidence: this reflects the level of trust and belief that the venture board has in the evidence presented by the teams for each of the questions in the various stages of the Product Lifecycle

- Potential future revenue:

Example metrics for Strategic innovation accounting

Current portfolio |

Innovation Results |

|---|---|

|

|

- Portfolio distribution: is a percentage-based representation of the types of ventures within your company. It shows the proportion of core offerings, adjacent ventures, and transformative ventures. These figures provide valuable insights into both the risk of disruption and strategic decision-making.

- Portfolio fade: this indicates the erosion or attrition rate of specific offerings within a portfolio. It indicates the extent to which these offerings are being diminished or phased out over time.

- Investment distribution: indicated the percentage of investments allocated to new ventures in each category core, adjacent, and transformational within your current investment portfolio. Providing insights into the strategic focus of your investments

- Net product viability index (NPVI): measures the percentage of total revenue generated from innovations introduced within the past five years. It serves as an indicator of the company's ability to generate revenue from recent product launches and assesses the vitality of its new product offerings.

- Cost of innovation: the total cost of the innovation funnel for a specific time period. This includes the combined expenses of live ventures, ventures in the sustain phase, and discontinued investments.

- Average time to sustain (ATS): This metric measures the average duration it takes for a venture within the innovation funnel to progress from its creation to the sustain phase. It provides an indication of the typical timeframe for ventures to achieve stability and sustainability within the innovation process.

- Average funnel conversion rate (ACR): this is the average "survivability" within the company's innovation funnel. It provides insight into the likelihood of an idea progressing to maturity. It answers the question of how many ideas are expected to reach fruition if a specific number is initiated today. This information is valuable in managing expectations for innovation investment and understanding the potential outcomes of the ideas being pursued.

- Efficiency of innovation investment: indicates how well our innovation converts into revenue. It can be calculated by dividing the total revenue generated in the current year from products launched within the past X years by the total costs incurred for innovation during the same X-year period. The specific timeframe for X can be determined based on the company's requirements and objectives.

Innovation Accounting articles

Today we will be talking about the “innovation accounting framework” that Esther and Dan introduced in their book Innovation Accounting. Things like employee’s skills and culture (that are intangible) are becoming more and more important for companies their in-market success. Organizations are more reliant on innovation to drive profit than ever before. A new, non-financial, […]

We see a lot of organizations that want to start tracking innovation performance by using innovation accounting. But where should you start? And what are the hurdles? Questions like these are very common and logical as we are just entering a new area of corporate innovation. In this blog, we will discuss what to do […]

We struggle to iterate quickly – I’d like to identify metrics to demonstrate that innovations are moving forward? This challenge from the first Group Call at Innov8ers really caught my eye. It is a struggle that we’ve seen a lot with both our own startups and the corporate startup teams that we’ve coached over the years. Especially […]

How to start with innovation accounting? We start with measuring the following three innovation KPIs from corporate startups.

Last weekend Diego Menchaca, founder of Teamscope and apparently also a big fan of our blog posts, proposed that I should write a blog post about Mixpanel. “Most blog posts tell what to track on Mixpanel, but it would be great to know what’s your approach when defining events and properties.” We love Mixpanel at […]

Yesterday we had the first introductory session with a potential portfolio company and tried once again to explain why it is so important to focus first on a clear early adopter. We often compare the early adopter with a person who fell of his bike (we’re from Amsterdam after all) and broke his arm. His […]

In the previous two posts we gave you an introduction to analytics, discussed vanity metrics and the criteria for good metrics. In this post we’d like to introduce the Pirate Metrics, an analytics framework created by Dave McClure of 500 startups. It’s called Pirate Metrics not just because Dave McClure seems to be a big […]

One of the most requested topics when mentoring startups are analytics. Startup founders know that they have to measure things and that analytics are the solution, but not a lot of people know how to actually apply it. The problem is that even after reading the books (like Lean Analytics, which I can highly recommend), it is still hard to apply to your own startup.